Green recovery through renewable energy auctions?

The complex finance of globalized energy markets in emerging economies

A little over a year ago, a major rolling blackout hit Argentina, leaving 50 million in the dark. To give some context, I wrote a vignette about the recent past and possible future of the country’s power grid, and its entanglement with the country’s ongoing financial and economic duress. I cited a study (Schaube et al. 2018) that was cautiously optimistic: experiments with (local and) renewable energy were taking place across the country, building capacity and creating a proper niche. If only the government would open up the energy and industrial markets a little more, so said the niche’s protagonists, and initiatives would flourish.

Fast forward and it’s been a tough year for the Argentinians. Previous president Macri’s bet on a combination of budget cuts and more borrowing didn’t pay off, while his nominally progressive successor duo Fernandez and Kirchner have not been able to stop the receding tide with increased social assistance. Just before the pandemic hit, the country was bankrupt, yet again. The peso took another nosedive, and while the relatively robust infrastructure of social assistance has enabled the country to avoid the worst of the pandemic’s consequences, the percentage of people living under the poverty line is expected to grow to near half (!) of the population.

“Covid 19 - Buenos Aires”, by Santiago Sito. Argentina recently struck a deal with its creditors.

Yet, despite all this, renewable energy capacity has grown substantially, and despite some delays due to lockdown measures, predictions are Argentina is still on track to meet its (admittedly modest) goals: 20% renewables by 2025. Interestingly, that’s not because local initiatives flourished. Instead, most of that growth comes from big foreign investment in solar and wind, through a national auction system called RenovAr. Basically, energy companies of different stripes bid to offer electricity for a certain amount of (MW) capacity for a certain price, and if they win the bid, they get to sell electricity under those conditions for a guaranteed amount of time, enough to recoup investment and make-a some-a-that-a monney.

Meanwhile, we need to ‘remobilize’ our economies after the lockdown ground many parts of it to a halt. You’ll have heard people advocating for a ‘green recovery’: cleaning up the economy as a way of reviving it better than it was. There is a rich country version of this idea – Let’s deficit-spend our way out of this mess! Money is cheap! – and a poor country version – Green industrialization is the way to go (for Latin-America)! Who’s got capital? Er, no one? Uhm, let’s borrow! Wait, sh*t, this money is expensive! 🤦♀️.

Enter, therefore, the auction. If national electricity institutions are no longer able to make the investments necessary to keep up with demand and to green the supply, you invite people that do have the capital to invest and give them a concession. And to make sure the price at which they’re willing to offer electricity is reasonably low, you actually don’t just politely invite, but you auction off your concession to the, well, lowest bidder.

Seems reasonable, no? For a country with troubled access to credit especially, such schemes look like they could prove a sturdy bootstrap. Indeed, auctions have been applied in various countries over the last few years and have been widely celebrated. Argentina’s RenovAr in fact received some accolades of its own, in particular for its effort to ‘de-risk’ energy investments (more on that later). Former undersecretary of Energy Sebastián Kind is generally recognized for setting up these auctions to be successful and as a consequence has been awarded with all sorts of honorary positions, while also receiving 2 million from the Packards’ Global Breakthrough Fund to replicate the model globally: GREENMAP.

Greenmap’s Master Plan.

So, are these auctions a good part of a green recovery mix? To answer that question, let’s set some criteria. Obviously, they have to be effective at increasing (renewable) energy supply (and in so doing reduce prices), but they must also generate opportunities for local or national economic development, whether that be in the form of industrial capacity or benefits for surrounding communities.

We’ll look at three cases: Mexico, South-Africa, and Indonesia. Each has been a recent ‘success story’, where auctions have led to substantial additions of wind and/or solar. Each country had a slightly different approach to the auctions, but you’ll see that we can observe similar reasons for success as well as similar pitfalls.

Mexico

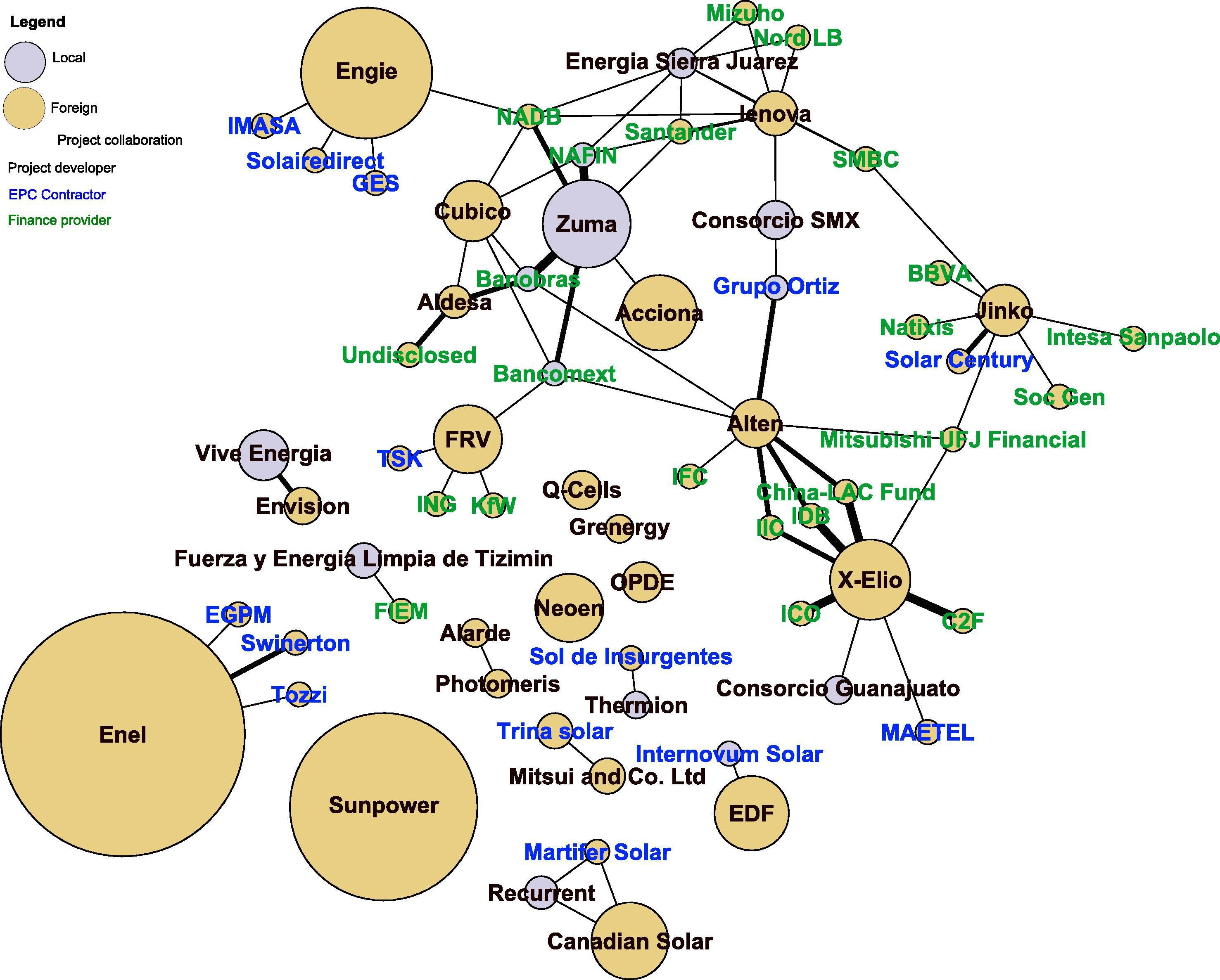

Mexico’s main objective was to add capacity at the lowest price, but it also hoped to boost local ‘green industry’. Its resolute focus on price appears to have created incentives for unrealistic bids, because the ‘attrition rate’ (unfinished developments) is quite high so far. Gringo and European energy companies won most (and the biggest) of the bids. While they did work with some local industry to produce some of the more straightforward parts (like rotor blades), they involved known foreign partners for the complex financial and legal questions, which require niche knowledge. So far, then, the record for new industrial capacity building is pretty poor. (Matsuo & Schmidt 2019)

Networks formed in the downstream value chain, image by Matsuo & Schmidt.

South-Africa

The standout characteristic for the South-African program is that the auction had a Black Economic Empowerment clause, which required companies to create local jobs and give communities 2.5% ownership. While these conditions were formally met (again, mostly by European companies, but also some Indian and Chinese players this time), again the complexity of these projects, the considerable social remove of the companies, and poor institutional support mean communities weren’t able to meaningfully make use of the revenue streams and jobs weren’t actually created (Sovacool et al 2019, see also this earlier issue on the economics of renewable energy in Southern Africa).

Indonesia

Government installed solar panels gives power to 36 houses in the village of Weepatando in Sumba island (Asian Development Bank).

While Indonesia has significantly jacked up its electrification rate in recent years, catching up with its regional neighbours, there were still some regions where electrification was trailing. It therefore created incentives for electrification in these regions, by pegging the ceiling for tariffs to local rates, which were lower in well-served regions, thus curbing potential profits there. Still, most of the projects wound up targeting these well-served regions, because that existing, proven (institutional) infrastructure also meant fewer risks in project development. Such safer bets were made by finance capital conglomerates that now included energy in their portfolio (a trend following suspiciously close on the heels of the 2009 financial crisis). Kennedy (2018) emphasizes the predominance of this logic with this kind of institutional investors:

project ‘bankability’ – the ability of a project to generate sufficient profit to satisfy lender requirements – has become the core metric against which project viability and desirability is judged.

The financialization of renewable energy

All of these countries were successful in attracting foreign capital to build out new grid capacity. That success comes with a sizeable asterisk though with regards to knock-on benefits. In great part this has to do with the financialization – “the expansion and proliferation of financial markets” (Baker 2015) – of renewable energy. That can mean:

The demands of project finance: impatient capital needs a lot of ‘de-risking’ and thus accepts a limited range of possible projects, excluding all the risky parts of local investments.

The predominance of Big Renewable: the alternative to project finance is the global energy conglomerate whose bankability is based on its many, many baskets of renewable eggs. Their capital is more patient, but their size seems to make it difficult for them to be local team players.

Financialization mitigates against the small scale of the niche that Schaube et al. were so hopeful for. The scale of the investments also makes it difficult for communities to get meaningfully involved, for instance as shareholders.

Of course, all of this could be a legitimate learning curve. We’re 5 years into most of these projects. More projects will follow, more “co-benefits” may yet transpire. Matsuo and Schmidt (2019) advocate tweaking economic ‘local content’ requirements, for these to actually encourage developing local supply chains. It is a careful dance that itself requires knowledge of what capacity is already out there, upon every auction round. For example, if there’s no base capacity to satisfy requirements, investors won’t propose projects. Something similar can be said for community co-benefits: it requires state institutional know-how to support communities in their self-representation and management of resources.

Still, tweaks can’t mitigate against the systemic reasons for the problem of scale, not anytime soon. For that, you need to change the system itself – you’d need, in other words, a sea change in the global political economy of sustainability.

Sources

None of this could have been written without the excellent work by the following authors. All sensible observations are theirs; all nonsense is mine. Obviously, there is much more to learn from them, so if I piqued your interest, click on the links below.

Baker, Lucy. 2015. "The evolving role of finance in South Africa's renewable energy sector". Geoforum. 64: 146-156. https://doi.org/10.1016/j.geoforum.2015.06.017

Kennedy, Sean F. 2018. "Indonesia’s energy transition and its contradictions: Emerging geographies of energy and finance". Energy Research & Social Science. 41: 230-237. https://doi.org/10.1016/j.erss.2018.04.023

Knuth, Sarah. 2018. "“Breakthroughs” for a green economy? Financialization and clean energy transition". Energy Research and Social Science. 41: 220-229. https://doi.org/10.1016/j.erss.2018.04.024

Slightly off-topic but read for how the Silicon Valley logic of venture capital completely missed what it would take to make sensible investments in ‘cleantech’ (and how cleantech is now morphing into fintech).

Matsuo, Tyeler, and Tobias S. Schmidt. 2019. "Managing tradeoffs in green industrial policies: The role of renewable energy policy design". World Development. 122: 11-26. https://doi.org/10.1016/j.worlddev.2019.05.005

Sovacool, Benjamin K., Lucy Baker, Mari Martiskainen, and Andrew Hook. 2019. "Processes of elite power and low-carbon pathways: Experimentation, financialisation, and dispossession". Global Environmental Change. 59. https://doi.org/10.1016/j.gloenvcha.2019.101985

Energy auctions are just one part of this article, so together with their tripartite analytical framework this is a great quick-and-dirty introduction into the topic if you need one.

PS:

If you do not have the appropriate credentials to cross the paywall to these articles, maybe you can check out https://sci-hub.tw (just copy paste in the doi number), or if you are uncomfortable with that, send me a message and I’ll lend you a copy.